Agribank’s loan book full of junk

AG Junias Kandjeke gave Agribank a qualified audit opinion for 2017 as he wasn’t satisfied with the bank’s provision for bad debts and credit control.

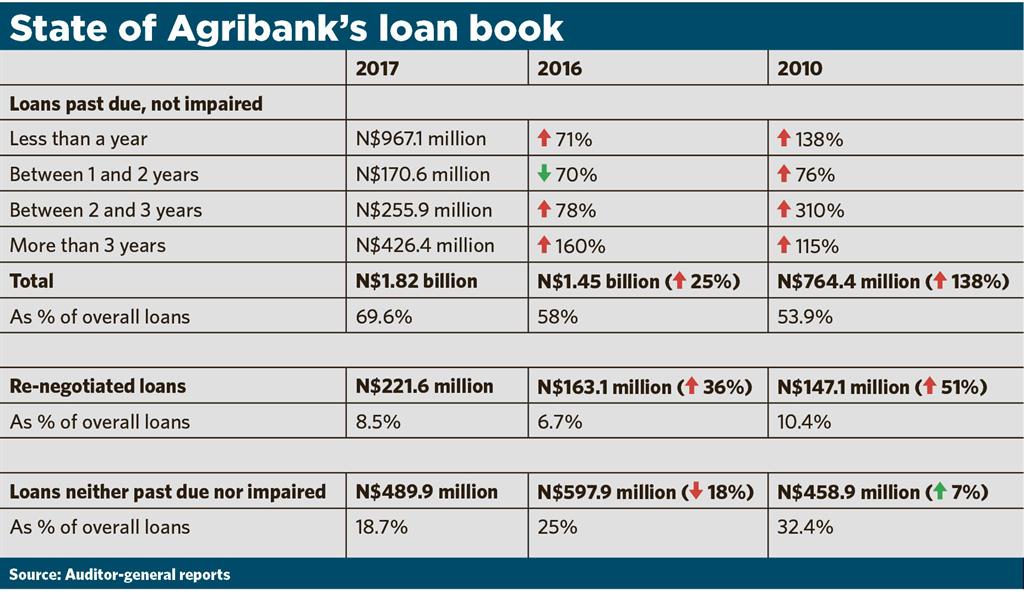

Jo-Maré Duddy – More than N$2 billion – or 78% of all Agribank’s loans – are either sub-standard, doubtful or a loss.

Only about N$489.9 million worth of loans were neither past due nor impaired at the end of March this year, auditor-general Junias Kandjeke says in his report on the bank latest set of financials.

“Healthy” loans - which in the 2016 book-year amounted to about N$597.9 million - dropped by 18% in the past financial year.

Loans past due but not impaired, on the other hand, escalated by nearly N$369 million or 25% to just less than N$1.82 billion. Loans of which the credit terms were re-negotiated, increased by 36% to nearly N$221.6 million.

Kandjeke gave Agribank a qualified audit opinion for 2017 as he wasn’t satisfied with the bank’s provision for bad debts and credit control. His report was tabled in the National Assembly this week.

During the financial year under review, Agribank adopted BID-2 - the Determination on Asset Classification, Suspension of Interest and Provision – to compute for the provision of bad debts. “With 78% of loans being graded in the sub-standard, doubtful and loss categories, the application of collateral values in calculating the provision is critical,” the AG said.

However, the accuracy and completeness of the collateral values on the system is “doubtful” because of “inadequate controls (monitoring, supervision and review)” over the capturing of the data, he said.

'No clear plan'

As an example Kandjeke cited 1 100 loan accounts with the total book value of about N$483.7 million which didn’t have their collateral values captured on the system by the end of March 2017. Although this was partially corrected off the system, collateral values for loans with a book value of more than N$36.8 million remained unrecorded.

In addition, no collateral values were allocated to the ring-fenced accounts that were created on the implementation of the drought relief scheme.

“There was no clear plan of action for capturing collateral – detailing timing of the project, supervision and monitoring process, as well as quality control checks. Though the process has been on-going since 2013, the collateral values of some loan accounts granted prior to 2013 are still not captured,” Kandjeke said.

The AG said Agribank’s credit quality has been worsening on an annual basis. He welcomed the bank’s decision to use debt collectors to recoup arrears, but said the effect of these efforts will only be felt in the 2018 financial year.

Kandjeke also pointed out that Agribank’s loans were under-secured by about N$318.2 million by the end of March this year. This represents 12% of its loan book. “This exposes the bank to the risk of losses in the event of debtors defaulting on payments,” he said.

Agribank’s loan book at the end of March totalled about N$2.6 billion.

Only about N$489.9 million worth of loans were neither past due nor impaired at the end of March this year, auditor-general Junias Kandjeke says in his report on the bank latest set of financials.

“Healthy” loans - which in the 2016 book-year amounted to about N$597.9 million - dropped by 18% in the past financial year.

Loans past due but not impaired, on the other hand, escalated by nearly N$369 million or 25% to just less than N$1.82 billion. Loans of which the credit terms were re-negotiated, increased by 36% to nearly N$221.6 million.

Kandjeke gave Agribank a qualified audit opinion for 2017 as he wasn’t satisfied with the bank’s provision for bad debts and credit control. His report was tabled in the National Assembly this week.

During the financial year under review, Agribank adopted BID-2 - the Determination on Asset Classification, Suspension of Interest and Provision – to compute for the provision of bad debts. “With 78% of loans being graded in the sub-standard, doubtful and loss categories, the application of collateral values in calculating the provision is critical,” the AG said.

However, the accuracy and completeness of the collateral values on the system is “doubtful” because of “inadequate controls (monitoring, supervision and review)” over the capturing of the data, he said.

'No clear plan'

As an example Kandjeke cited 1 100 loan accounts with the total book value of about N$483.7 million which didn’t have their collateral values captured on the system by the end of March 2017. Although this was partially corrected off the system, collateral values for loans with a book value of more than N$36.8 million remained unrecorded.

In addition, no collateral values were allocated to the ring-fenced accounts that were created on the implementation of the drought relief scheme.

“There was no clear plan of action for capturing collateral – detailing timing of the project, supervision and monitoring process, as well as quality control checks. Though the process has been on-going since 2013, the collateral values of some loan accounts granted prior to 2013 are still not captured,” Kandjeke said.

The AG said Agribank’s credit quality has been worsening on an annual basis. He welcomed the bank’s decision to use debt collectors to recoup arrears, but said the effect of these efforts will only be felt in the 2018 financial year.

Kandjeke also pointed out that Agribank’s loans were under-secured by about N$318.2 million by the end of March this year. This represents 12% of its loan book. “This exposes the bank to the risk of losses in the event of debtors defaulting on payments,” he said.

Agribank’s loan book at the end of March totalled about N$2.6 billion.

Kommentaar

Republikein

Geen kommentaar is op hierdie artikel gelaat nie