Prospects all downhill in 2009, say experts

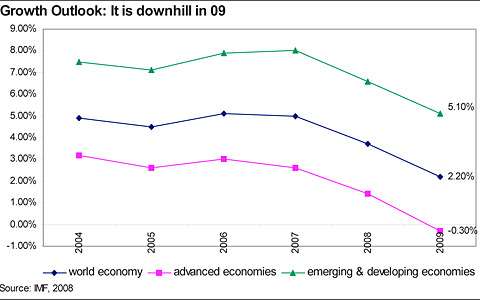

THE year 2008 has been quite a year, aside from Barack Obama being elected as US president. The world economy underwent what is rightly considered one of the worst financial crises since possibly the 1930’s. Mid-year it was widely expected that the world economy will slow to a growth rate of 3.7% this year. This expectation is still intact.

However, in 2009 we will feel the full impact of the global financial crisis across the globe. The IMF has recently revised their growth outlook for 2009 down to 2.2%. Even this may however prove optimistic given the enormity of the current crisis. Growth in advance economies will slow significantly and may even contract further.

Similarly, the growth outlook for emerging economies remains bullish but a slowdown is expected as export earnings comes under pressure. In fact, the IMF revised their growth outlook down by 1% percentage point in November. The IMF projects a growth rate of 5.1% for emerging and developing economies. Thus most economies will grow below potential for 2009 with minimal recovery towards 2010 as investment demand reacts to better liquidity and risk appetite.

Currently, in the international financial markets effective credit extension is limited because of risk aversion. Indicative of the bank risk aversion risk spreads have widened across a broad range of financial assets. For example, the so-called TEDspread which measures the degree to which US banks are willing to lend to each other has widened since September 2008 to 300 basis points.

However, there are signs that the spread is narrowing to below 150 basis points as of the 22nd December. Nevertheless, it will certainly take some time before credit extension recovers to pre-crisis levels, notwithstanding creative policy measures by Central Banks to restore confidence in credit markets. A slowing world economy means a slowing Namibian economy. Namibia’s major trading partner economies are slowing with further downside risk to the growth outlook.

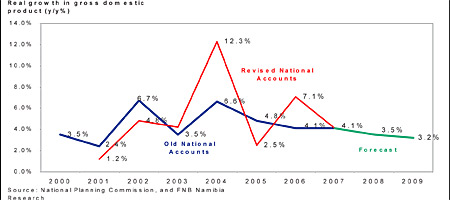

In fact, most of Namibia’s export destination, from Spain to the UK, will experience negative growth in 2009. Therefore, we maintain our view that economic growth will fall to 3.2% in 2009. This is slightly optimistic compared to the recently announced IMF Article IV missions’ view of 2% growth. However, there are pertinent risks to our growth outlook given the challenges experienced in the mining sector.

If the recently reported direct and indirect labour-shedding in the mining sector materializes then the knock-on effect on private consumption expenditure and thus the growth outlook will be great. Furthermore, worryingly the recently rebased National Accounts for 2007 by the Central Bureau of Statistics show that investment demand fell by 4.2% between 2006 and 2007, in real terms, mainly as real investment in the mining and quarrying sector fell by 47.26% over the same period.

Falling mineral prices do not auger well for future mining investment growth. Thus the key risk for future economic expansion is a slowing private sector investment demand, particularly in mining. Therefore the economic outlook is one of subdued growth.

Consumer oriented sectors, especially wholesale and retail trade, accommodation, finance and real estate, will increasingly feel the effects of falling household demand, notwithstanding the recent interest rate cut as the real economy adjusts to the changing global demand and supply conditions. Therefore, mining and manufacturing are likely to remain weak due to the current export demand shock as recession deepens in importing economies and mineral prices falls further.

– FNB Namibia Research Brief December 2008

However, in 2009 we will feel the full impact of the global financial crisis across the globe. The IMF has recently revised their growth outlook for 2009 down to 2.2%. Even this may however prove optimistic given the enormity of the current crisis. Growth in advance economies will slow significantly and may even contract further.

Similarly, the growth outlook for emerging economies remains bullish but a slowdown is expected as export earnings comes under pressure. In fact, the IMF revised their growth outlook down by 1% percentage point in November. The IMF projects a growth rate of 5.1% for emerging and developing economies. Thus most economies will grow below potential for 2009 with minimal recovery towards 2010 as investment demand reacts to better liquidity and risk appetite.

Currently, in the international financial markets effective credit extension is limited because of risk aversion. Indicative of the bank risk aversion risk spreads have widened across a broad range of financial assets. For example, the so-called TEDspread which measures the degree to which US banks are willing to lend to each other has widened since September 2008 to 300 basis points.

However, there are signs that the spread is narrowing to below 150 basis points as of the 22nd December. Nevertheless, it will certainly take some time before credit extension recovers to pre-crisis levels, notwithstanding creative policy measures by Central Banks to restore confidence in credit markets. A slowing world economy means a slowing Namibian economy. Namibia’s major trading partner economies are slowing with further downside risk to the growth outlook.

In fact, most of Namibia’s export destination, from Spain to the UK, will experience negative growth in 2009. Therefore, we maintain our view that economic growth will fall to 3.2% in 2009. This is slightly optimistic compared to the recently announced IMF Article IV missions’ view of 2% growth. However, there are pertinent risks to our growth outlook given the challenges experienced in the mining sector.

If the recently reported direct and indirect labour-shedding in the mining sector materializes then the knock-on effect on private consumption expenditure and thus the growth outlook will be great. Furthermore, worryingly the recently rebased National Accounts for 2007 by the Central Bureau of Statistics show that investment demand fell by 4.2% between 2006 and 2007, in real terms, mainly as real investment in the mining and quarrying sector fell by 47.26% over the same period.

Falling mineral prices do not auger well for future mining investment growth. Thus the key risk for future economic expansion is a slowing private sector investment demand, particularly in mining. Therefore the economic outlook is one of subdued growth.

Consumer oriented sectors, especially wholesale and retail trade, accommodation, finance and real estate, will increasingly feel the effects of falling household demand, notwithstanding the recent interest rate cut as the real economy adjusts to the changing global demand and supply conditions. Therefore, mining and manufacturing are likely to remain weak due to the current export demand shock as recession deepens in importing economies and mineral prices falls further.

– FNB Namibia Research Brief December 2008

Kommentaar

Republikein

Geen kommentaar is op hierdie artikel gelaat nie